February 12, 2023

How much should you have saved before buying a house? Tips on planning for your first house purchase.

Tips to help you plan for buying a first home

Buying your first home is often one of the biggest milestones in life and can be an extremely exciting but daunting experience. But as long as you manage your finances and plan carefully, it can become a much smoother process.

The very first step in this very long journey is knowing how much you should have saved in order to afford the house. Needless to say, this figure will vary significantly depending on the type of house you’re looking to purchase but we recommend sticking within the range of 15 to 20% of your deposit PLUS some extra fees listed below:

Stamp Duty

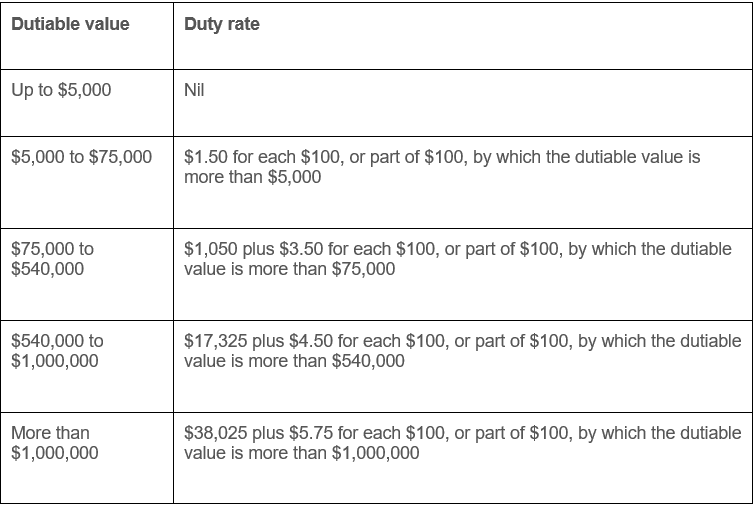

All property sales in Queensland involve stamp duty which depends on the market value of the property or the price paid for the property (whichever is higher) including GST. While both parties of a sales transaction are liable to pay stamp duty but this cost is usually covered by the purchaser.

Fortunately, first time home buyers are not liable to pay stamp duty for properties with a value of up to $500K and qualify for a discounted rate on properties valued between $505K and $550K.

If the property you’re purchasing is valued more than that, check the rates below or use this handy stamp duty calculator.

(Table Source: https://qro.qld.gov.au/duties/transfer-duty/calculate/rates/)

If you’re struggling to pay for stamp duty, check out if you are eligible for these exemptions or concessions: first home concession, first home vacant land and home concession.

Or if check out these schemes specifically for first time home buyers check out these schemes: First Home Super Save Scheme (FHSSS) and First Home Guarantee Scheme (FHGS).

Lenders Mortgage Insurance (LMI)

If you’re only able to afford a deposit that is less than 20% of the purchase price, you’ll also have to pay for LMI. This insurance is in place to protect the lender in the event that you are not able to make loan repayments and the lender is unable to recover the loan balance.

This is a one-off fee and can vary depending on which bank you choose. While the average LMI fee is $6,200, we recommend putting aside 2% of the amount borrowed.

For more information, check out the Insurance Council of Australia's website.

Due Diligence Costs

This section includes costs such as inspections and legal fees. While this may not seem like an important step, it’s best not to skip this step as it can not only give you a peace of mind but potentially also save you a ton of money in the future.

In general, these checks would cost you around $2,000 - $5,000.

Bank Fees

Other bank related fees such as loan establishment fees, document fees or bank valuations could cost you between $1,000 to $2,000.